The Architecture of Modern Private Credit: Operational Strategies for Real Estate and Specialty Finance in 2026

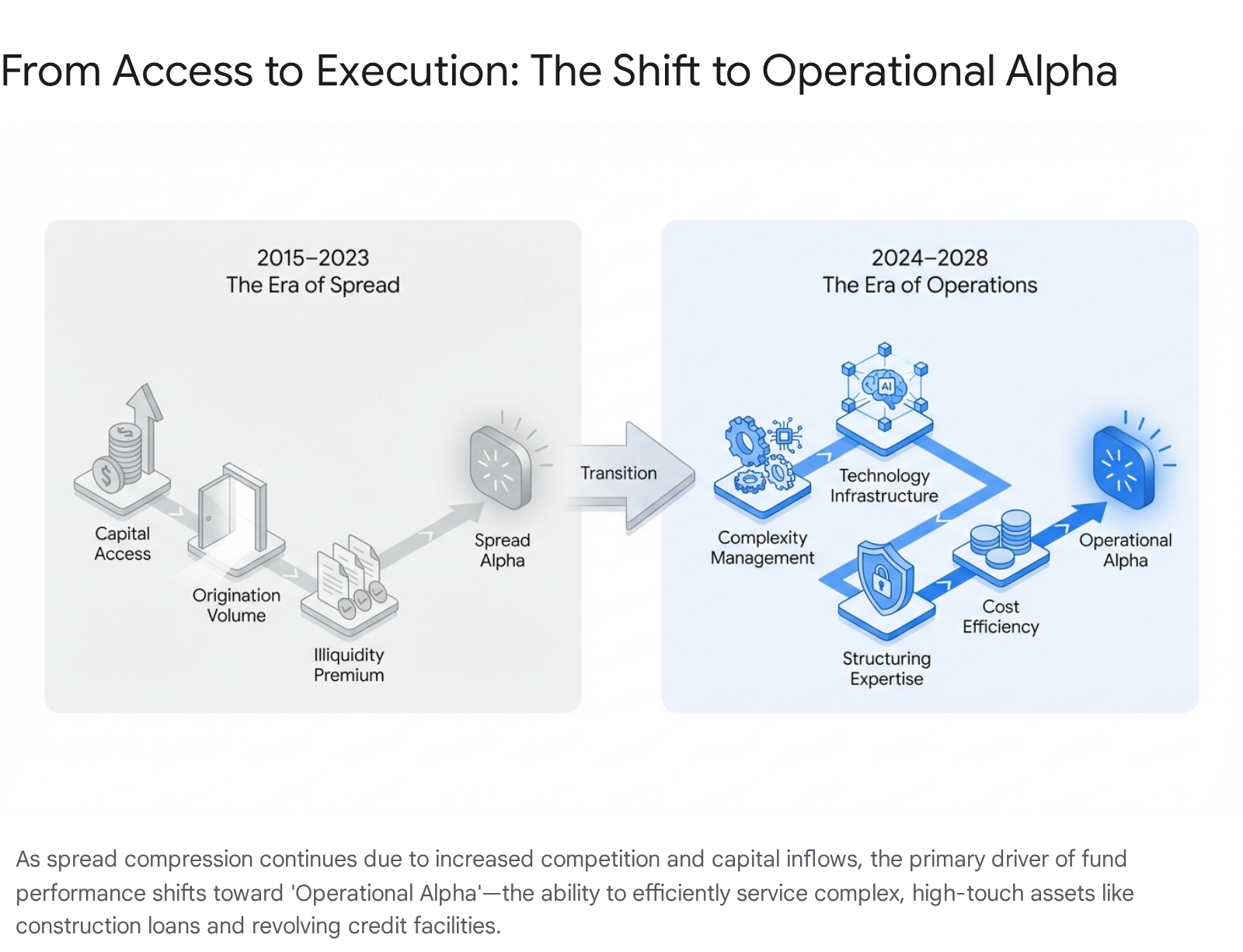

Executive Strategic Overview: The Era of Operational Alpha

The financial landscape of the mid-2020s is witnessing a profound structural transformation: the decoupling of credit origination from traditional depository institutions. This is not merely a cyclical fluctuation but a secular shift driven by the "Basel III Endgame" and the subsequent regulatory tightening following the regional banking liquidity crises of 2023. By early 2026, private credit has evolved from a niche "shadow banking" activity into a primary pillar of corporate and real estate finance, with assets under management (AUM) surging past the $1.7 trillion mark and projected to approach $3 trillion by 2028.1

However, the “golden era” of easy spread capture is over. As the market matures, the source of outperformance is shifting. In the early 2020s, returns were driven by the illiquidity premium and widening spreads. In 2026, with competition compressing yields and a massive “maturity wall” looming over commercial real estate, the differentiator for fund managers is no longer just access to deal flow, it is Operational Alpha.

Operational Alpha is the ability to execute complex, high touch lending strategies, especially in Business Purpose Lending and Asset Based Lending, with the speed and efficiency of a fintech while maintaining the disciplined controls of a global bank. It requires a re-architecture of the operating stack: moving away from rigid legacy systems built for the “happy path” toward modern, event-driven platforms that can handle the real world of construction draws, borrowing base volatility, and multi-layered syndication waterfalls. The best operators pair automation with auditability, enforcing structured intake validation before data becomes official, and structured release assurance before any statements, remittances, or investor reporting leaves the platform.

The private credit borrower is no longer defined solely by distress or an inability to secure bank financing. Today, private credit serves as the financing engine of choice for real estate developers, small-to-mid-sized enterprises (SMEs), and specialized industries ranging from agriculture to logistics. These borrowers prioritize speed, certainty of execution, and structural flexibility over the lowest possible cost of capital. Consequently, the lenders serving them—debt funds, family offices, and specialty finance companies—require technology infrastructure that can handle complex, bespoke deal structures that rigid, legacy core banking systems were never designed to support.1

This report analyzes the operational bifurcations of the private credit market, the specific friction points in BPL and ABL, the lessons learned from recent high-profile fraud cases, and the technological roadmap for 2026 and beyond.

Part I: The Macro-Structural Landscape of 2026

To understand the operational imperatives of 2026, one must first grasp the macroeconomic and regulatory forces that have reshaped the terrain. The market is defined by three converging pressures: the regulatory retreat of traditional banking, the looming maturity wall in commercial real estate, and the aggressive expansion of private credit into the retail wealth channel.

The Basel III Endgame and the Banking Retreat

The regulatory environment of 2026 is defined by the finalized implementation of Basel III reforms, often termed the "Basel III Endgame." While recent political shifts have led to speculation about a "capital neutral" implementation under the new administration, the structural impact on bank behavior is largely irreversible.7 Traditional banks, burdened by increased capital requirements for risk-weighted assets and heightened scrutiny on deposit flight risk following the 2023 regional banking crisis, have significantly retrenched from non-standardized lending.1

The "Endgame" rules specifically penalize holding complex, illiquid assets on the balance sheet. For banks, the capital charge for holding a non-investment grade corporate loan or a transitional real estate loan has increased to the point where the Return on Equity (ROE) is no longer competitive. This retreat has catalyzed a massive migration of borrower demand toward the private markets, fundamentally altering the mechanisms of capital formation in the global economy.1

This retreat has created a permanent vacuum in the middle-market and specialty finance sectors. Banks are increasingly shifting to an "originate-to-distribute" model or partnering with private credit firms rather than holding complex loans on their balance sheets.10 For private credit managers, this is a double-edged sword: it provides a robust pipeline of deal flow but also introduces new risks as "lender-on-lender" violence becomes common in restructurings. In today's market, survival depends less on documentation alone and more on strategic positioning within the capital stack to avoid being "primed" or structurally subordinated by aggressive maneuvering from other creditors.9

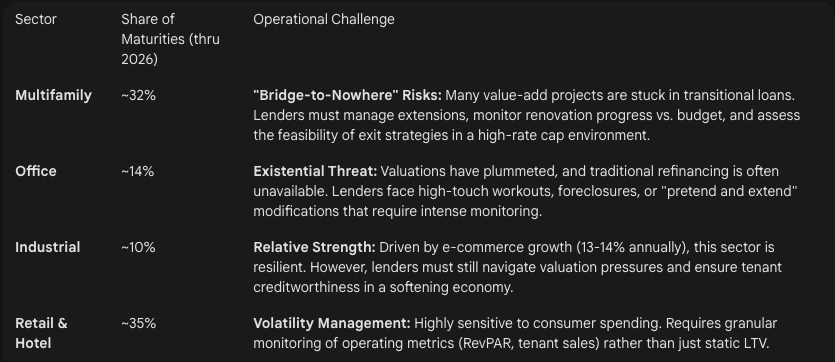

The $1.5 Trillion Maturity Wall

The private credit market is currently navigating a massive "maturity wall" in commercial real estate (CRE) debt. Approximately $1.26 trillion to $1.5 trillion in commercial real estate loans are set to mature through 2027.4 The structural challenge here is the disparity in interest rate environments. Most of these maturing loans were originated in the low-rate environment of the mid-2010s to early 2020s, with interest rates averaging between 4.1% and 4.7%. In 2026, refinancing these assets occurs in a rate environment closer to 6.5% to 7.0%, creating a significant gap between debt service costs and property cash flow performance.4

This "wall" is not a monolith but a rolling series of sector-specific challenges, each requiring distinct operational capabilities from lenders:

Data Sources: 5

For private lenders, this environment demands a shift from passive "servicing" (collecting payments) to active "asset management." The ability to manage extensions, loan modifications, workouts, and enforcement actions at scale is now a critical competency. Lenders who lack the data infrastructure to identify "at-risk" loans months before maturity will face severe portfolio deterioration.1

The Retailization of Private Credit

A defining trend of 2026 is the "retailization" or democratization of private credit. Fund managers are aggressively tapping into the private wealth channel—mass affluent and high-net-worth investors—through semi-liquid structures like evergreen funds, interval funds, and non-traded business development companies (BDCs).13

This shift fundamentally alters the operational requirements of a fund. Unlike institutional capital which is typically locked up for 10 years in closed-end funds, retail capital requires a significantly more robust back-office infrastructure:

Liquidity Mechanisms & Cash Drag: Semi-liquid funds typically offer periodic liquidity (e.g., up to 5% of the fund's NAV per quarter). This requires precise cash management to meet potential redemptions without forcing fire sales of illiquid assets. Managers must maintain a "liquidity sleeve" or secure credit lines to manage this mismatch.16

Valuation Velocity: Retail investors and regulators demand more frequent and transparent valuations. While institutional funds might mark assets quarterly, retail products often require monthly or even near-real-time Net Asset Value (NAV) calculations. This velocity is impossible if the underlying loan data is trapped in PDFs or spreadsheets.15

Reporting Scale: Servicing thousands of individual investors requires automated reporting infrastructures. The manual generation of capital account statements is no longer scalable. Technology must automate the distribution of personalized performance data and tax documents.1

Part II: The Operational Bifurcation – BPL vs. ABL

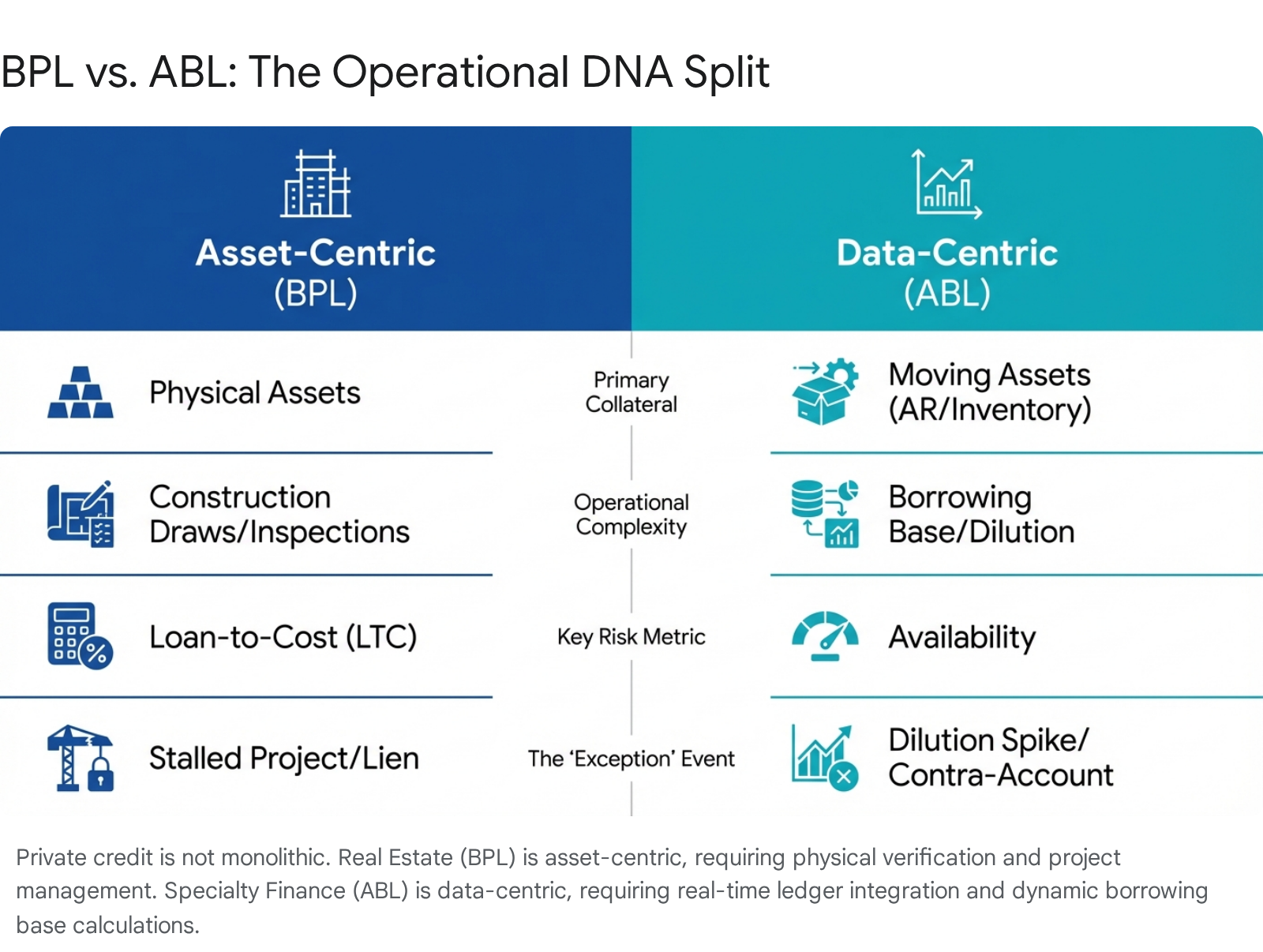

To effectively operate in this market, one must recognize that "Private Credit" is not a monolithic asset class. It is sharply divided into two distinct ecosystems with differing operational DNA, risk triggers, and data requirements: Real Estate Private Credit (Business Purpose Lending - BPL) and Specialty Private Credit (Asset-Based Lending - ABL). A technology platform or operational strategy that attempts to treat them identically will inevitably fail.1

1. Real Estate Private Credit (BPL): The Asset-Centric Challenge

Real Estate Private Credit, often categorized under Business Purpose Lending (BPL), explicitly serves investors rather than owner-occupiers. This distinction is critical because it exempts these loans from many consumer protection regulations (such as TRID and Ability-to-Repay rules), allowing for faster origination and more aggressive servicing. However, the servicing requirements are far more intensive than a standard 30-year fixed mortgage due to the transitional nature of the collateral.1

The Construction Finance Bottleneck

Construction finance is the operational heavyweight of BPL. Unlike a standard mortgage where the full loan amount is funded at closing, construction loans differ fundamentally because funds are "drawn" over time as work is completed. This creates a "negative cash flow" dynamic where the lender is constantly disbursing cash rather than collecting it. The loan balance increases over time, and interest is typically calculated on the outstanding balance, requiring sophisticated "interest reserve" management.1

The Servicing Nightmare: The Draw Process

The draw process is the single most significant friction point in BPL lending. It is a multi-party workflow involving the borrower, the general contractor (GC), the lender, and a third-party inspector, all operating with misaligned incentives.

The Draw Request: The borrower submits a request for funds (e.g., $50,000 for framing and foundation). This request must be supported by a "Schedule of Values" (SOV)—a detailed line-item budget—and evidence of work, such as invoices and lien waivers.

The Inspection: The lender dispatches a third-party inspector to the site to verify the physical progress. The critical question is not just "is it done?" but "is the percentage complete commensurate with the funds requested?"

The Reconciliation: The lender must reconcile the inspector's report (Physical % Complete) with the borrower's request (Financial % Spent). This is rarely a perfect match.

The Discrepancy (The Pain Point): If the inspector reports that only 40% of the framing is complete, but the borrower is requesting payment for 50%, the draw must be "cut" or rejected. This leads to disputes, delays, and potential work stoppages, which in turn jeopardizes the project's timeline and the lender's collateral.

The Disbursement: Once approved, funds are wired. To mitigate the risk of funds diversion, prudent lenders often pay the subcontractors directly, adding another layer of payment processing complexity.1

Technological Gaps: Most lenders still manage the Schedule of Values in Excel. This disconnects the budget from the loan servicing system. If a change order moves $10,000 from "Roofing" to "Foundation," the Excel sheet is updated, but the system of record often is not. This leads to massive reconciliation errors at loan payoff. Furthermore, inspection reports often arrive as PDF attachments, requiring manual data entry that slows funding velocity.1

Lien Waiver Management: Before releasing a draw, the lender must collect "Lien Waivers" from contractors to ensure they waive their right to place a mechanics' lien on the property. This is a document management challenge of the highest order. A modern platform should have the capability to block a draw payment automatically if the corresponding Lien Waiver is missing from the file. The industry is moving toward automated lien waiver exchange platforms to mitigate this risk.18

Residential Transition Loans (RTLs), colloquially known as "fix-and-flip" loans, are short-term, high-yield instruments designed to bridge the gap between acquisition and stabilization. These loans typically have terms ranging from 12 to 24 months. The primary value proposition of an RTL lender is speed. In a competitive housing market, borrowers often need to close in 10-14 days to win bids against cash buyers. Lenders struggle to balance this velocity with the necessity of adequate underwriting, including valuation and title work.1

Extension Risk and Modification Fatigue: With the housing market softening in certain regions and rates remaining "high for longer," borrowers are increasingly failing to execute their exit strategies (sale or refinance) by the loan maturity date. This leads to a high volume of loan modification and extension requests. Servicers are inundated with the administrative burden of processing these extensions, which involves re-underwriting the asset, collecting extension fees, and generating legal modification documents.1

Cross-Collateralization Complexity: Professional real estate investors often borrow against multiple properties within a single loan facility to maximize leverage. Legacy systems often struggle to track a single loan secured by five different addresses, each with its own valuation, lien priority, and release clauses. The inability to seamlessly release a single property from a cross-collateralized pool upon its sale is a frequent operational bottleneck.1

Securitization Drivers: The validity of RTLs as an institutional asset class has been affirmed by the increasing volume of securitizations. Rated RTL securitization volumes surpassed $7 billion in 2024. For a servicing platform, this means that data output must meet the rigorous standards of rating agencies like KBRA and DBRS Morningstar. Fields that were once optional—such as "original property condition," "renovation timeline," and "contractor credit score"—are now mandatory for reporting.1

DSCR (Debt Service Coverage Ratio) Loans

DSCR loans are long-term (30-year) rental loans underwritten based on the property's cash flow (rent vs. expenses) rather than the borrower's personal income (DTI). They are effectively the BPL equivalent of a standard mortgage for professional investors.

Prepayment Penalties: Unlike consumer mortgages, DSCR loans almost always carry "Yield Maintenance" or "Step-down" prepayment penalties (e.g., 5-4-3-2-1%). The servicing system must automatically calculate these complex fees if a borrower pays off early. Errors in this calculation can lead to significant revenue leakage for the lender.

Escrow Administration: Like traditional mortgages, DSCR loans often require tax and insurance escrows. However, because these are commercial loans, the insurance policies are often complex "blanket" policies covering multiple properties. The servicing system must be able to track these complex insurance relationships and disburse payments accurately.1

2. Specialty Private Credit (ABL): The Data-Centric Challenge

While Real Estate credit relies on the value of a place, Specialty Finance relies on the velocity of commerce. This vertical—often called Asset-Based Lending (ABL)—finances the working capital cycle of businesses. The collateral is liquid and fleeting: an invoice that will be paid in 30 days, or inventory that will be sold next week. The lender’s security depends entirely on the accurate monitoring of these fluctuating assets.1

The Core Mechanism: The Borrowing Base

Unlike a mortgage where the loan amount is static, an ABL facility is a living, breathing organism. The "Borrowing Base" determines how much credit is available on any given day.

Dilution Risk: Dilution refers to the difference between the face value of an invoice and the cash actually collected. If a borrower issues an invoice for $100, but the customer returns $10 worth of goods, the "real" value is only $90. This $10 reduction is "dilution." Lenders must calculate dilution dynamically to ensure they aren't lending against phantom value. If dilution rises from 2% to 5%, the lender is suddenly over-advanced.1

Contra-Accounts: A major risk in ABL is when the borrower also buys from their customer. If Borrower A owes Customer B $50, and Customer B owes Borrower A $100, Customer B might only pay the net $50. The lender, expecting $100, is left short. Identifying these "contra-account" relationships in thousands of ledger entries is a massive data challenge that requires sophisticated software logic.1

Supply Chain Finance & Ag-Tech

Specialty finance is increasingly moving into niche verticals like agriculture, where perishability adds a "ticking clock" to the collateral. For example, platforms like ProducePay finance fresh produce, a sector historically underserved by banks due to volatility. The risk isn't just credit; it's biology. If the strawberries rot in transit, the collateral value hits zero. To mitigate this, lenders in this space need "logistics-aware" servicing. They integrate with shipping trackers (like GPS on trucks) and weather data. If a shipment is delayed, the lending platform might automatically downgrade the collateral value or trigger a risk alert. This represents the bleeding edge of "Specialty Credit"—where loan servicing merges with supply chain management.1

Servicing Nuances: The Daily Grind

Daily Reconciliations & Lockboxes: In ABL, the lender often controls the cash to mitigate risk. Customers pay directly into a "Lockbox" owned by the lender. The lender must then receive the cash, "Apply" it to the specific invoice (Cash Application), reduce the outstanding loan balance, and release any excess cash to the borrower.

The "Unapplied Cash" Problem: If a payment of $5,000 comes in with no reference number, it sits in "Unapplied Cash." While it sits there, the borrower's loan balance isn't reduced, interest keeps accruing, and the borrower relationship suffers. Automation that uses OCR and AI to match payments to invoices is a critical "pain killer" feature, reducing the manual labor of reconciliation from weeks to days.1

Part III: The Fraud Frontier – Lessons from the Field

The opacity of private credit, combined with legacy operational practices, has created vulnerabilities that bad actors exploit. The years 2025 and 2026 have seen significant fraud cases that highlight the necessity of independent data verification and the dangers of relying on borrower-generated reporting.

Case Study 1: First Brands Group – The Double Pledge

In late 2025, First Brands Group, a major aftermarket auto parts supplier, filed for bankruptcy amid explosive allegations of massive fraud. The company accrued over $2.3 billion in factoring liabilities based on "fabricated" or "doctored" invoices, shocking the private credit market.23

The Mechanism: The company allegedly utilized "double-pledging" or "duplicate financing," a scheme where the same invoices were used to secure financing from multiple lenders simultaneously. Furthermore, investigations revealed that inventory pledged as security to one lender (Evolution Credit Partners) may have been commingled with collateral securing a separate asset-backed loan facility managed by Bank of America.25

The Failure: The core failure lay in the reliance on borrower-provided Borrowing Base Certificates (BBCs) without sufficient independent verification. In the absence of a centralized, immutable registry for pledged receivables, the borrower was able to arbitrage the information gap between disparate lenders. The lack of real-time integration with the borrower's ERP allowed the fabrication to continue undetected until the liquidity crisis became terminal.1

Case Study 2: Carriox Capital – The Fabrication Factory

Carriox Capital, a New York-based receivables financing firm, collapsed in a high-profile Chapter 11 filing after it was revealed that its owner had fabricated telecom receivables to secure over $552 million in loans from major institutional investors, including HPS Investment Partners (a subsidiary of BlackRock).27

The Mechanism: The fraud was sophisticated and deeply entrenched. The scheme involved forging contracts, creating fake email domains to impersonate legitimate customers (such as T-Mobile and Telstra), and even building fake websites to mislead auditors during due diligence checks.29

The Lesson: "Trust but verify" is insufficient in modern ABL. Lenders cannot rely on the borrower's digital paper trail or surface-level diligence. Direct, API-based integration with the borrower's invoicing system and independent third-party verification of the end-debtor are the only robust defenses against this level of sophisticated fabrication. The Carriox case serves as a stark warning: when trust in intermediaries collapses, the damage ripples far beyond a single balance sheet.30

These cases underscore that fraud happens in the data gaps. When lenders rely on PDF reports, manual reconciliations, and periodic audits, they lack the real-time visibility to detect duplicate pledges, dilution spikes, or fabricated receivables until it is too late. The operational mandate for 2026 is clear: Data Sovereignty. Lenders must own the data pipe, not just read the report.

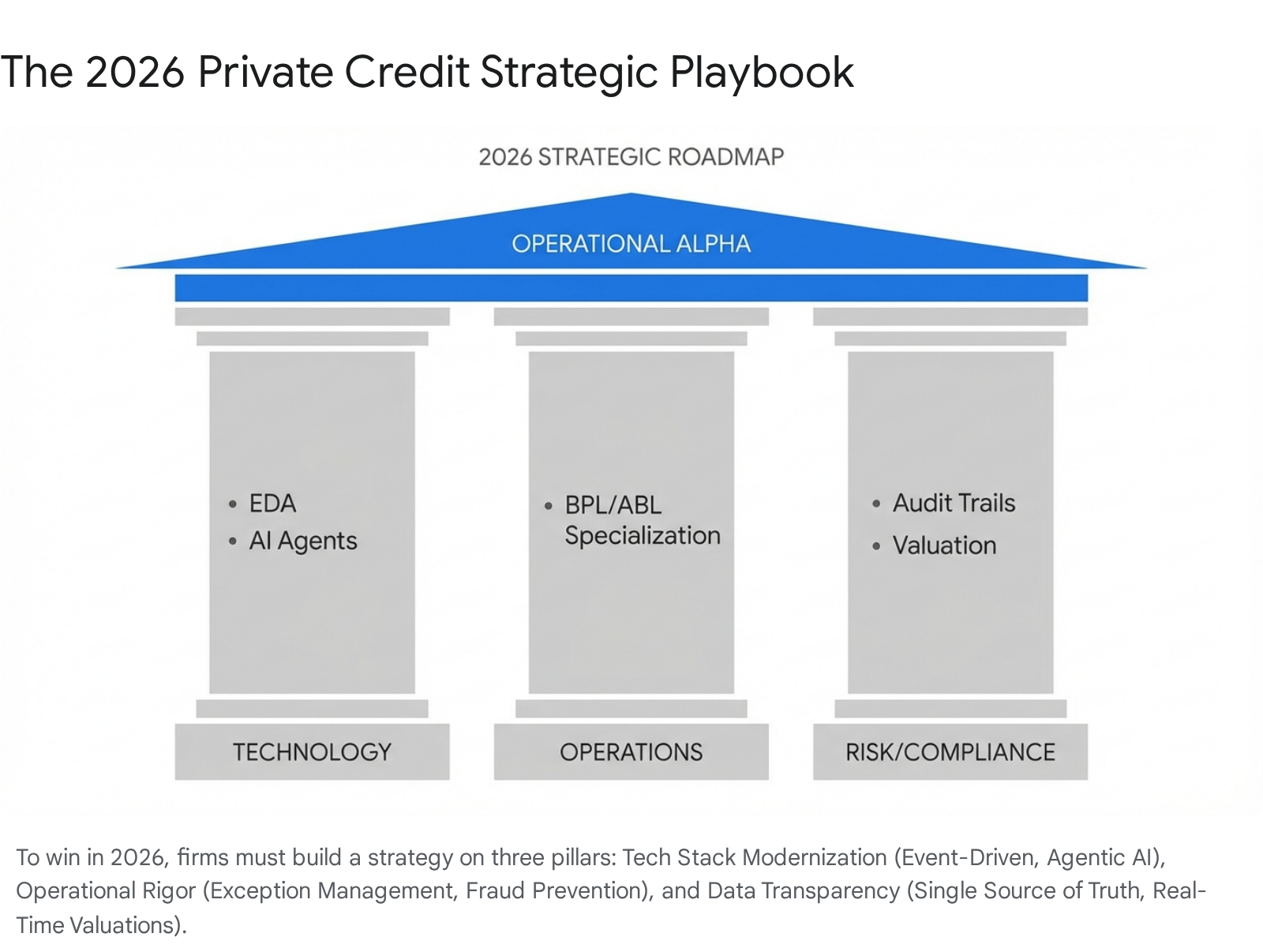

Part IV: The Technology Stack Transformation

To survive the "Operational Alpha" era and mitigate the fraud risks exemplified by First Brands and Carriox, private credit lenders must retire the "Excel-to-System" bridge. The market opportunity for a new loan servicing platform exists because the incumbent technology stack is failing. Lenders are trapped between rigid legacy cores that are too broad, and ad-hoc spreadsheets that are too risky.1

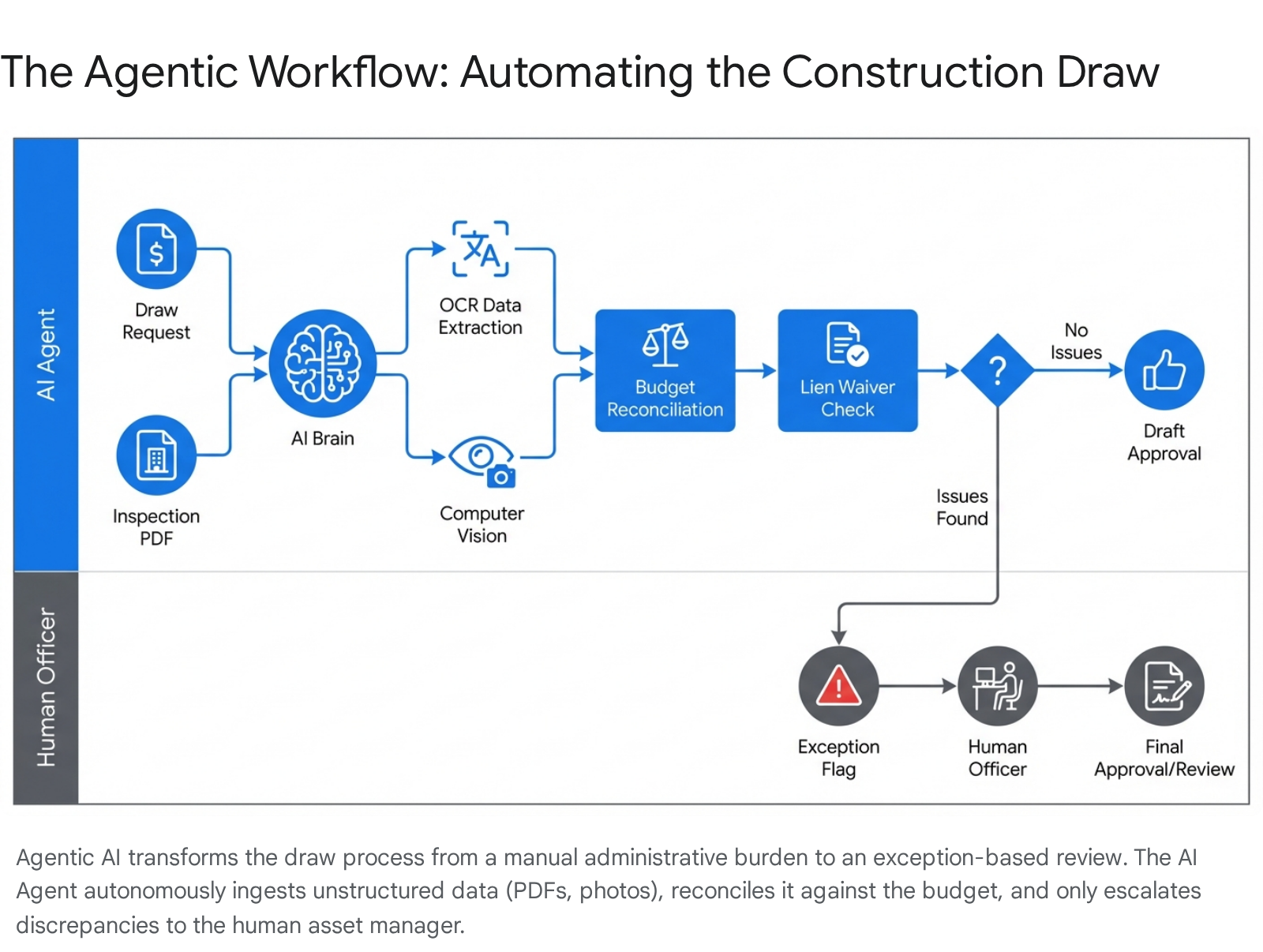

1. The Rise of Agentic AI

By 2026, Artificial Intelligence in lending has moved far beyond "GenAI" (summarizing text) to Agentic AI—autonomous agents capable of reasoning, planning, and executing complex workflows with minimal human intervention.33

The "Draw Agent": A prime example of this evolution is the "Draw Agent" launched by Built Technologies. This agentic workflow automates the construction draw process—historically a manual bottleneck. The agent reviews inspection reports, reconciles them with the budget, checks for lien waivers, and drafts the approval decision. Early adopters report reducing processing time by up to 95%, transforming a review that took hours into one that takes minutes.35

Autonomous Workflows: Unlike rigid "If/Then" rules, AI agents can handle ambiguity. For instance, if an inspection report contains a photo of a "50% complete" foundation but the invoice claims "60%," the agent can flag the discrepancy, draft a query to the inspector, and propose a "cut" to the draw amount, waiting for human sign-off. This "human-in-the-loop" model allows lenders to scale their portfolio without linearly scaling headcount.36

2. Data Mesh & The "Single Source of Truth"

As private credit firms expand into multiple strategies (Direct Lending, Real Estate, ABL, Infrastructure), data silos become a significant liability. The Data Mesh architecture is emerging as the solution for 2026.38

Concept: Instead of trying to force all data into a monolithic data warehouse, Data Mesh treats data as a "product" owned by specific domains. For example, the Real Estate team owns property data, while the Credit team owns borrower financial data.

Application: This allows for a federated governance model where data is accessible via standardized APIs across the firm. An investment committee member can pull a real-time report that combines property valuations (from the RE domain) with borrower credit scores (from the Credit domain) without needing to manually reconcile disparate spreadsheets. This enables real-time cross-asset risk analysis and supports the complex reporting needs of institutional LPs.38

3. Blockchain for Fraud Prevention

In response to the double-pledging scandals, blockchain technology is finally finding a pragmatic use case in preventing invoice fraud. Decentralized ledgers are being used to create a "single source of truth" for pledged receivables. By tokenizing invoices, lenders can verify authenticity and uniqueness instantly, ensuring that an invoice hasn't already been pledged to another lender. While industry-wide adoption is still evolving, platforms leveraging blockchain for invoice verification are gaining traction as a necessary risk mitigation tool.40

Part V: Regulatory & Compliance Pressures

The "Wild West" days of private credit are essentially over. The regulatory environment is shifting from "hands-off" to "active monitoring," driving specific feature requirements for servicing software.

The Aftermath of the Private Fund Adviser Rules

Although the Fifth Circuit Court of Appeals vacated the SEC's prescriptive Private Fund Adviser Rules in June 2024, the market has effectively adopted the core principles of transparency as a standard. The ruling removed the federal mandate, but it did not remove the investor demand.42

"Regulation by LP": Limited Partners (LPs), particularly sophisticated institutional investors, are using their leverage to enforce the transparency that the SEC failed to mandate. Side letters are increasingly requiring quarterly statements with detailed fee breakdowns and preferential treatment disclosures.44

Operational Impact: Funds must tag every fee (Origination Fee, Servicing Fee, Exit Fee) with metadata so it can be automatically rolled up into these reports. Manual compilation of these reports is no longer scalable or acceptable to LPs. The expectation is "institutional-grade" reporting, regardless of the regulatory baseline.1

Level 3 Asset Valuation Scrutiny

Private credit loans are typically "Level 3" assets—illiquid and hard to value. In a high-interest-rate environment, valuations are heavily scrutinized by investors and auditors.

The Valuation Challenge: Auditors no longer accept "Cost" (par value) as the default valuation. They want to see a Discounted Cash Flow (DCF) model based on current credit performance.

Tech Role: The servicing platform must feed real-time performance data (delinquency status, DSCR trends, LTV changes) directly into the fund's valuation engine. If a borrower misses a payment, the asset's "Fair Value" might drop by 2%. The speed of this information flow is critical for accurate NAV (Net Asset Value) reporting, especially for semi-liquid funds where stale valuations can lead to arbitrage by redeeming investors.1

Audit Readiness & Immutable Logs

With the SEC's continued focus on "off-channel communications" and ad-hoc adjustments, an immutable Audit Trail is non-negotiable. Every change—an interest rate adjustment, a waived late fee, a draw approval—must be logged with a user stamp and timestamp. Legacy spreadsheets lack this control, making them a significant liability in an audit scenario. A robust "change log" is now a defensive necessity.1

Part VI: Strategic Recommendations for Marketing the Platform

To market a loan servicing platform to this sophisticated audience in 2026, you must pivot the conversation from "features" to "risk mitigation" and "operational alpha." The buyer is not just looking for a calculator; they are looking for an operating system for their business.

1. Sell "Exception Management," Not Just "Servicing"

The Pitch: "Your current system handles the 90% of loans that pay on time. We handle the 10% that don't."

Feature Focus: Highlight automated workflows for draw rejections, covenant breaches, and workout scenarios. Show how the system guides a junior analyst through a complex default process without needing to call a partner. This resonates with managers who are worried about "key person risk" in their operations.1

2. Position "Data Ingestion" as a Competitive Advantage

The Pitch: "Stop turning your credit analysts into data entry clerks."

Feature Focus: Showcase the API connectivity and OCR capabilities. Demonstrate how the platform ingests a messy Rent Roll or a scanned Borrowing Base Certificate and instantly calculates the DSCR or Availability. This appeals to the COO/CFO who is trying to scale AUM without scaling headcount linearly.1

3. The "Shadow System" Killer

The Pitch: "Retire the spreadsheets that keep you up at night."

Feature Focus: Target the "Shadow Ledger"—the Excel sheets used for construction budgets and syndication waterfalls. Position the platform as the "Single Source of Truth" that eliminates the reconciliation gap between the Servicing System and the General Ledger.1

4. Vertical-Specific Modules

For Real Estate: Market a "Construction Command Center" that integrates inspection photos with draw requests.

For Specialty Finance: Market a "Dynamic Borrowing Base Engine" that calculates dilution in real-time.

Strategy: Do not sell a generic "Loan System." Sell a specialized tool that understands the nuance of their specific asset class. The "one size fits all" approach is viewed with skepticism in this market.1

Conclusion

The private credit market of 2026 is defined by its complexity. The simple loans have stayed with the banks or moved to standardized fintechs. What remains in the private credit universe are the difficult, high-touch, data-intensive deals: the ground-up construction projects, the complex inventory revolvers, and the multi-lender syndications.

In this environment, a loan servicing platform wins in this market not by being a better calculator, but by being a better operator. It must be the nervous system that connects the physical reality of the asset (the building, the invoice) with the financial reality of the fund (the waterfall, the audit). By solving for the specific friction points of BPL and ABL—Draws, Dilution, and Data—the platform ceases to be a utility and becomes a strategic partner in the lender's growth.

%201-p-500.png)

.avif)