The Sovereign Operating Model: Structuring Private Credit for Operational Alpha, Control, and Scalability

Private credit is outgrowing its infrastructure. This report introduces the Sovereign Operating Model—a hybrid framework that bridges the "Middle Office Gap" by combining in-house control with outsourced scalability.

The global financial architecture is undergoing a structural transformation of historic magnitude. Private credit, once a niche alternative asset class utilized primarily for distressed situations or highly specific mezzanine financing, has matured into a cornerstone of the modern capital markets. Current projections estimate the market will swell to between $2.3 trillion 1 and $3.5 trillion 2 by 2028, fundamentally altering the mechanism of capital allocation for middle-market companies and real estate investors alike. This shift is not merely cyclical; it is a secular trend driven by the long-term retrenchment of traditional banking institutions, accelerated by regulatory tightening and the need for more flexible, bespoke capital solutions.3

However, this explosive growth has exposed a critical fracture in the industry’s infrastructure, a phenomenon we identify as the "Middle Office Gap." As deal volumes scale and the complexity of loan structures increases—incorporating hybrid debt-equity features, complex draw schedules, and intricate covenant packages—private lenders face a paradoxical challenge. To scale effectively, they require the robust, institutional-grade infrastructure typically associated with large commercial banks. Yet, to maintain their competitive advantage—which relies on speed, flexibility, and deep, high-touch borrower relationships—they cannot afford the bureaucratic inertia, high fixed costs, or loss of control associated with traditional bank servicing models or legacy outsourcing providers.

For the emerging generation of private lenders—ranging from family offices and high-net-worth syndicates to specialized debt funds—the operational burden scales non-linearly. A portfolio of fifty loans may be manageable with spreadsheets and a diligent operations manager. A portfolio of five hundred loans, however, becomes an operational minefield where manual processes fail, data integrity degrades, and the risk of significant financial error multiplies.5

This report introduces a transformative approach to resolving this dilemma: the Hybrid Technology-Enabled Servicing Model. Derived from the operational philosophy of Bedrock Core™, this model rejects the binary choice between "building in-house" (which incurs high fixed costs and operational distraction) and "outsourcing completely" (which results in the loss of data sovereignty and brand dilution). Instead, it proposes a co-sourcing framework where the lender retains the "Front Office" functions—borrower relationships, strategic decision-making, and brand presence—while integrating a specialized partner to manage the "Back Office" execution—loan accounting, data integrity, and workflow automation—via a shared, cloud-native technology backbone.

By adopting this hybrid architecture, lenders can achieve "Operational Alpha"—value generated not just through investment selection, but through superior execution, data control, and borrower retention.7 This report provides an exhaustive analysis of the macro trends driving this shift, deconstructs the mechanics of the hybrid model, and offers a strategic roadmap for implementation.

Chapter 1: The Macro Context and the Operational Crisis

1.1 The Great Retrenchment and the Rise of Private Capital

To understand the operational imperative facing today's private lenders, one must first contextualize the macroeconomic environment. The landscape of lending has shifted dramatically since the Global Financial Crisis (GFC) of 2008. In the aftermath of the GFC, and further compounded by the regional banking turmoil of 2023, traditional banks have systematically retreated from the middle-market lending space.3

This retreat is driven by a confluence of factors. Regulatory frameworks, such as Basel III and its subsequent iterations (often termed the "Basel III Endgame"), have imposed stringent capital requirements on banks, making it increasingly capital-intensive to hold certain types of corporate and real estate loans on balance sheets.8 Furthermore, the consolidation of the banking sector—the number of U.S. banks declined by 53% between 2000 and 2023—has reduced the number of institutions focusing on bespoke, relationship-driven lending.1

Into this void, private credit has stepped in as a vital provider of liquidity. Private lenders, unencumbered by the same regulatory capital constraints as depository institutions, can offer the speed, flexibility, and customized terms that modern borrowers demand.9 This has led to a surge in assets under management (AUM) and a diversification of strategies, from direct lending and distressed debt to asset-based finance and hybrid capital solutions.8

However, the "shadow banking" label often applied to this sector is becoming a misnomer. As the sector matures, it is moving out of the shadows and into the spotlight of regulators and institutional investors. This transition brings with it a heightened expectation for operational rigor. Institutional investors (Limited Partners or LPs), including pension funds and insurance companies, now demand the same level of transparency, reporting accuracy, and risk management from private credit funds as they do from public market investments.11 The "wild west" era of private lending is over; the era of institutionalization has begun.

1.2 The Middle Office Gap: Where Growth Meets Friction

While capital flows into private credit have been robust, the infrastructure to manage that capital has lagged significantly. This disconnect creates what we term the "Middle Office Gap."

In the lifecycle of a loan, the "Front Office" handles origination, underwriting, and borrower relationships. The "Back Office" handles the final accounting and settlement. The "Middle Office" is the messy, complex layer in between: it involves the ongoing administration of the loan, covenant monitoring, draw management, interest rate resets, and the coordination between the deal team and the finance team.13

As private credit funds scale, a fissure emerges between deal velocity and operational capacity. While deal teams are incentivized to close transactions rapidly, the operational infrastructure often remains static, relying on legacy systems or manual processes that cannot keep pace. This gap creates significant operational risk. When a fund grows from managing $100 million to $500 million, the complexity does not increase linearly; it increases exponentially. A spreadsheet that worked for 20 loans breaks down under the weight of 200, leading to data errors, missed billing cycles, and a lack of real-time visibility into portfolio health.5

This friction is not merely an administrative nuisance; it is a destroyer of value. Inefficiencies in loan operations can lead to "leakage"—lost revenue due to incorrect fee calculations or missed rate resets—and can severely damage the borrower relationship if service levels decline.15 Moreover, as the complexity of deals increases—with features like Payment-in-Kind (PIK) toggles, variable interest rates, and multi-tranche structures—the manual burden of tracking these variables becomes unsustainable.16

1.3 The "Adverse Selection" of Operational Focus

A critical insight from recent market research is the phenomenon of operational "adverse selection" within private lending firms. The principals of these firms are typically investment professionals—deal makers, underwriters, and credit analysts. Their expertise and passion lie in finding and structuring deals, not in managing the minutiae of loan administration.15

Consequently, the "Back Office"—servicing, payment processing, accounting, and covenant monitoring—is often treated as a secondary priority. Resources are allocated primarily to the revenue-generating Front Office, leaving the operations team understaffed and under-equipped. This neglect leads to the accumulation of "technical debt." Processes are patched together with ad-hoc solutions, and data is siloed in disparate systems (e.g., the CRM, the accounting software, and individual Excel files).14

The consequences of this operational adverse selection are severe:

Data Inconsistency: Without a centralized system of record, discrepancies arise between what the deal team believes the portfolio is yielding and what the accounting team records. This "data fog" hampers strategic decision-making and creates friction during audits.14

Borrower Friction: Borrowers in the private market pay a premium for speed and flexibility. If a lender cannot produce a payoff statement accurately within hours, or if payment applications are delayed, the borrower relationship degrades. In a market where repeat business is a key driver of growth, poor service is a competitive disadvantage.5

Compliance Risk: As scrutiny from capital providers on non-bank lenders increases, the lack of robust audit trails and standardized processes exposes the firm to significant legal and reputational liability.11

1.4 The Limitations of Binary Choices

Historically, lenders attempting to solve the Middle Office Gap have faced a binary choice: Build or Buy. Neither option fully addresses the needs of the modern private lender.

Option A: The "Build" (In-House) Trap

Building a full-service back office in-house offers maximum control but comes at a prohibitive cost.

High Fixed Costs: It requires hiring specialized loan accountants, servicing managers, and IT staff. These costs are fixed, meaning the lender pays them regardless of deal volume or revenue performance.19

Key Person Risk: In a small operations team, the departure of a primary loan administrator can result in a catastrophic loss of institutional knowledge. Training replacements is time-consuming and costly.13

Distraction: Every hour leadership spends managing servicing software implementations or hiring operations staff is an hour lost on capital formation and deal origination.

Option B: The "Buy" (Traditional Sub-Servicing) Trap

Outsourcing to a traditional sub-servicer offers scale but typically demands a total surrender of the borrower experience.

Brand Dilution: The borrower stops interacting with the lender and starts interacting with a third-party call center. The lender becomes a commodity capital provider rather than a strategic partner. This loss of touchpoints reduces the lender's ability to cross-sell or secure repeat business.20

Data Opacity: The lender loses real-time access to their data, often relying on static monthly reports rather than live dashboards. This "black box" servicing model prevents proactive risk management.14

Rigidity: Traditional servicers, often built to handle homogenous residential mortgages, are frequently ill-equipped to handle the bespoke, high-touch nature of private credit deals, such as complex construction draws or hybrid debt structures.16

The conclusion is clear: neither the purely in-house model nor the traditional outsourcing model fits the needs of the high-growth, relationship-driven private lender. A third way is required—one that combines the control of the in-house model with the scalability and expertise of the outsourced model.

Chapter 2: The Hybrid Architecture – Technology-Enabled Co-Sourcing

2.1 Defining the Hybrid Model

The solution to the operational dilemma lies in a hybrid operating model, often referred to in advanced financial circles as "Co-Sourcing" or "Component Servicing." This model, exemplified by the Bedrock Core™ framework 22, unbundles the lending value chain to optimize for both efficiency and control.

In this architecture, the lender retains the high-value, high-touch components of the relationship—specifically the borrower-facing interactions and strategic decision-making—while the partner provides the industrial-grade infrastructure to execute the low-value, high-risk operational tasks. This is not a simple vendor relationship; it is a strategic partnership where the technology platform acts as the bridge between the two entities.23

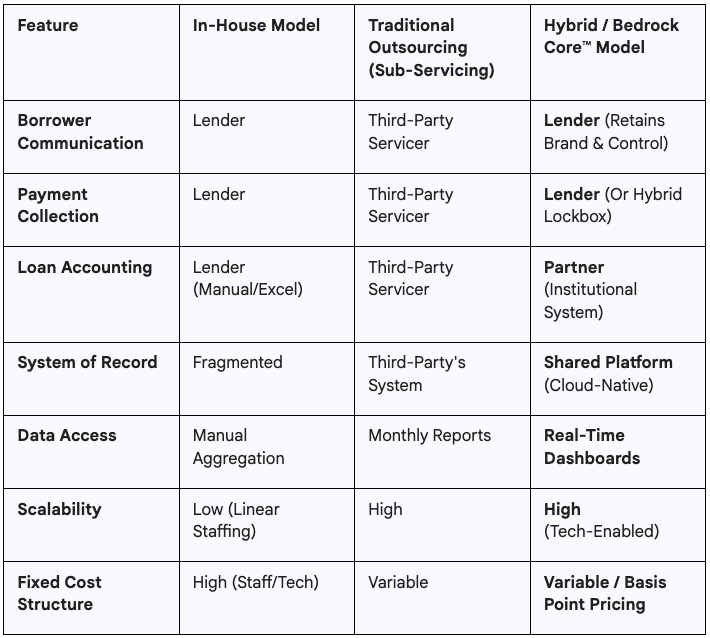

Table 1: The Hybrid Model vs. Traditional Models

This comparison highlights the fundamental shift: the Hybrid Model allows the lender to operate like a bank without building a bank. It provides the "backbone" of a major financial institution while preserving the agility of a boutique fund.22

2.2 The Bedrock Philosophy

Bedrock is designed to support a private lending program with technology-enabled servicing operations and loan accounting, ensuring that the operating foundation scales in lockstep with the portfolio without adding complexity or distracting from momentum.

The Commercial Terms of the Hybrid Deal: The structure is designed to align incentives. Instead of a flat fee that encourages the servicer to minimize work, or a per-loan fee that fails to account for complexity, the model utilizes a Servicing & Platform Fee based on Basis Points (bps) of the Committed Amount.22

Alignment: This aligns the partner’s revenue with the lender's growth. As the portfolio (AUM) grows, the infrastructure scales automatically, and the costs scale proportionately.

Predictability: The lender converts a volatile fixed cost (hiring staff, IT upgrades) into a predictable variable cost (bps fee or per loan fee).

Efficiency: By billing on "Committed Amount" rather than just "Drawn Balance" 22, the partner is compensated for the readiness and availability of the platform. This ensures that resources are always staged for rapid capital deployment—a key requirement for opportunistic private credit funds that need to move quickly when a deal presents itself.

2.3 Deconstructing the Division of Labor

To understand how this model offers "Control" and "Ease," we must examine the specific allocation of duties proposed in the hybrid framework. The model is predicated on a clear separation of "Front Office" and "Back Office" responsibilities.22

2.3.1 The Lender's Domain (The "Front Office")

Under the hybrid model, the lender explicitly acknowledges that the partner is not operating as a "borrower-facing outsource servicer" in the traditional sense.22 Instead, the Lender retains the critical touchpoints that define the client experience:

Borrower Communications: The lender remains the primary point of contact for the borrower. Whether it is responding to payoff requests, insurance follow-ups, or general inquiries, the borrower interacts with the lender's team. This ensures the borrower feels the "white glove" service of a private bank, rather than being routed to an impersonal call center.25

Collections & Default Management: The lender retains responsibility for borrower default management, including collections, outreach, and any legal or workout activities. This strategic discretion is vital in private credit, where relationships often span multiple deals. A lender may choose to be lenient with a repeat borrower facing a temporary cash flow crunch, a nuance that a rigid third-party servicer might miss.26

Brand Presence: All notices, statements, and portal interactions typically carry the Lender’s Brand, or are presented in a way that reinforces the lender's identity. The partner operates as a "white label" or invisible support structure.27

2.3.2 The Partner's Domain (The "Back Office Backbone")

The partner (Bedrock) operates as the "engine room," invisible to the borrower but essential to the lender. Their scope of services includes 22:

Loan Onboarding: This includes data mapping, validation, and cutover assistance. Onboarding is often the most labor-intensive and error-prone phase of any loan lifecycle. The partner's specialized expertise ensures that data is entered correctly from the start, preventing the "garbage in, garbage out" problem that plagues many self-serviced portfolios.14

Activity Tracking: The partner manages the back-office servicing operations, tracking loan activity, servicing events, and workflow management. This includes recording interest accruals, principal paydowns, and drawdowns in a sub-ledger system.

Loan Accounting & Reconciliation: Perhaps the most critical value-add is the support for loan accounting. The partner provides standard journals, reconciliation, and period-close tie-out support. This allows the lender’s finance team (CFO/Controller) to sign off on the books with confidence, knowing that the underlying data has been professionally reconciled.22

Technology Provision: The partner delivers the platform itself—including branded Lender Portals for authorized users, dashboards, loan-level views, and document access. This technology layer provides the transparency that makes the hybrid model possible.

Controls and Audit Support: The partner supports controls and audit trails, often implementing "maker-checker" or dual control workflows. This adds a layer of governance that is difficult to replicate in a small in-house team.22

Chapter 3: Operational Alpha – The Strategic Value Proposition

In the competitive private credit space, "Operational Alpha" refers to the additional value generated not through investment selection, but through superior operational execution.7 As yields compress and competition for deals intensifies, operational efficiency becomes a key differentiator. The Hybrid Model is a primary driver of this alpha, impacting speed, data sovereignty, and borrower retention.

3.1 Speed of Execution and "Deal Certainty"

Private credit borrowers often pay a premium for speed and certainty of execution. In the "fix-and-flip" or bridge lending space, the ability to close a loan in days rather than weeks is often the deciding factor for a borrower.29 A lender bogged down by manual back-office processes cannot compete on speed.

The Bottleneck: In manual environments, the same personnel often manage both new loan closings and existing loan draws. This creates a resource conflict; when deal volume spikes, servicing quality suffers, or conversely, servicing demands slow down new originations.

The Solution: By offloading the "servicing backbone" to a partner, the lender’s internal team is freed to focus purely on origination and underwriting.30 The partner’s infrastructure is "always on," scalable, and ready to onboard complex loan structures without the lender needing to hire new staff for every incremental $50 million in AUM. This elasticity ensures that the lender can seize market opportunities without being constrained by operational bandwidth.

3.2 Data Sovereignty and the "Golden Record"

One of the most profound advantages of the Hybrid/Co-Sourcing model is the retention of data ownership. In traditional outsourcing models, data effectively "leaves the building" and resides in the servicer's proprietary black box. Lenders receive static PDF reports or delayed data dumps, making it difficult to run ad-hoc analytics or integrate loan data with broader fund accounting systems.14

The Bedrock Approach: The Hybrid Model provides a randed Lender Portal 22 and direct access to data. This creates a "Golden Record"—a single, immutable source of truth for loan performance that is shared between the lender and the partner.

Real-Time Decisioning: Lenders can view exposure concentrations, liquidity requirements, and covenant compliance in real-time, rather than waiting for month-end reports. This immediacy is crucial for risk management in volatile markets.5

Audit Readiness: With "loan accounting and reconciliation support" included 22, the lender is perpetually audit-ready. The system generates the audit trail automatically, removing the frantic scramble that typically precedes an annual financial review or an investor due diligence request.

Shadow Accounting Elimination: Because the lender has direct visibility into the partner's system (or the system is effectively shared), there is no need for "shadow accounting"—the practice of maintaining a duplicate set of books to verify the servicer's numbers. This eliminates a major source of administrative waste and data reconciliation errors.31

3.3 The "White Glove" Retention Strategy

Borrower retention is the new battleground in mortgage and private lending. Market data suggests that retention rates vary significantly by execution, and banks/credit unions often outperform independent mortgage banks because they maintain a more holistic relationship.18 It costs roughly five times more to acquire a new client than to retain an existing one, and repeat borrowers bring significantly more revenue on average.34

The Friction of Outsourcing: When a loan is transferred to a mega-servicer, the borrower experience often plummets. They become a number in a massive database. If they encounter hardship or have a complex question, they navigate a rigid Interactive Voice Response (IVR) system and speak to a different agent every time. This creates a disconnect that makes it easy for the borrower to shop elsewhere for their next loan.20

The Hybrid Advantage: By retaining "borrower-facing responsibilities" 22, the private lender keeps the relationship warm. When a borrower needs a payoff statement or has a question about a draw, they call the banker who funded the deal—the person who understands their business plan. This touchpoint is not a burden; it is an opportunity to originate the next loan.

Repeat Business: Private lenders, especially in the real estate sector, rely heavily on repeat borrowers (e.g., developers doing multiple projects). The Hybrid Model ensures that the servicing experience reinforces the lending relationship, rather than severing it. It allows the lender to leverage their brand equity throughout the lifecycle of the loan.34

Chapter 4: The Financial Architecture of the Hybrid Model

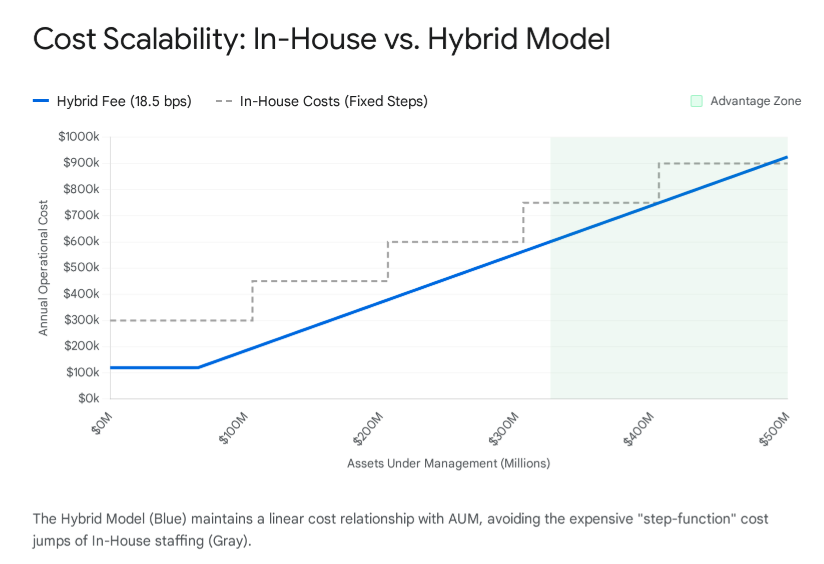

Adopting a hybrid model is not just an operational decision; it is a fundamental restructuring of the lending firm’s financial architecture. It transforms the cost structure from a rigid, high-fixed-cost model to a flexible, scalable variable-cost model.

4.1 Converting Fixed Costs to Variable Costs

Building an in-house servicing operation requires significant upfront capital (CapEx) for software licenses and ongoing operating expense (OpEx) for salaries and benefits.

Software Costs: Enterprise-grade loan servicing software is expensive. License fees, implementation costs, and customization can run into the hundreds of thousands of dollars. Maintenance and updates add to this burden annually.35

Personnel Costs: A competent loan servicing manager and a loan accountant are specialized roles. Their combined salaries and benefits can easily exceed $200,000 to $300,000 annually. Crucially, these are fixed costs. The lender pays these salaries whether the fund has $10 million in loans or $100 million, and whether the market is booming or stagnant.19

The Hybrid Economics: The Bedrock pricing structure 22 utilizes a basis point (bps) model (e.g., roughly 17-20 bps) applied to the Committed Amount.

Scalability: Costs grow only as the revenue-generating asset base grows. A startup fund pays a low minimum fee; a billion-dollar fund pays a fee commensurate with its scale and revenue. This "pay-as-you-grow" model protects the lender's margins during the early stages of growth.

Efficiency Ratio: This keeps the lender’s efficiency ratio optimized. The "One-Time Setup Fee" (often waived for longer terms) and reasonable "Minimum Monthly Fee" provide a low barrier to entry compared to the cost of hiring a single full-time employee and licensing enterprise-grade software.22

No Idle Capacity: In an in-house model, if deal flow slows, the operations staff sits idle, dragging down profitability. In the hybrid model, the cost base adjusts (to the extent that AUM fluctuates), or at least remains aligned with the potential revenue represented by the committed capital.

4.2 Mitigating the "Hidden Costs" of Errors

The cost of servicing is not just the monthly fee or salary; it is also the cost of errors and risk.

Leakage: In manual or poorly managed systems, "leakage" is common. This includes missed interest rate resets (especially in a rising rate environment), incorrect fee calculations (late fees, extension fees), or failed draw tracking. Even a small error rate can bleed basis points of yield from a portfolio over time.14

Remediation: Fixing a year’s worth of bad accounting data is incredibly expensive. Forensic accounting charges to restate books can cost multiples of the annual servicing fee.

The Expert Layer: The Hybrid Model leverages "disciplined operational execution led by former commercial banking operations professionals".22 This expertise acts as an insurance policy against operational leakage. The partner assumes the responsibility for getting the math right, backed by institutional-grade systems that have automated checks and balances.

Chapter 5: Risk Management, Compliance, and Governance

5.1 Segregation of Duties and Internal Controls

A core principle of internal control and fraud prevention is the segregation of duties. In a small private lender shop, it is common for the same person (or a small group of partners) to originate the loan, approve the draw, and record the entry in the books. This concentration of authority creates a significant fraud risk and potential for error.

The Hybrid Solution: The Bedrock model inherently introduces an external "Maker-Checker" workflow. While the lender ("Maker") may authorize a draw or a change in loan terms, the partner ("Checker") processes the accounting entry and validates the data against the loan documents and system rules.22

Dual Control: This structure creates a system of dual control. The partner acts as an independent verifier of the transaction. This external validation layer provides significant comfort to LPs and auditors, demonstrating that the fund’s reported performance is backed by an independent third party's records.22

5.2 Disaster Recovery and Business Continuity

Operational resilience is a critical component of risk management. Lenders must ask themselves: If their office is hit by a natural disaster, or if their local server goes down, or if they suffer a ransomware attack, can they continue to service their loans and report to investors?

Institutional Resilience: By utilizing a partner like Bedrock, the lender effectively outsources a significant portion of their IT and disaster recovery risk. The partner provides "Data backup, retention, and disaster recovery procedures" as part of the service level agreement.22

SOC Compliance: Institutional partners typically operate within a SOC-compliant infrastructure (Service Organization Control), which adheres to rigorous standards for security, availability, and confidentiality. For a small or mid-sized lender to build and maintain a SOC-compliant IT environment in-house is often cost-prohibitive. Accessing this infrastructure through a partner is a highly efficient way to upgrade the firm's security posture.35

5.3 Managing Complexity and "Hybrid" Structures

Private credit deals are becoming increasingly complex. "Hybrid" loans—which may combine senior debt, subordinated debt, and equity kickers, or include complex PIK (Payment-in-Kind) toggles—are growing in popularity as lenders seek to bridge valuation gaps.16

Managing these structures requires sophisticated tracking. A manual error in calculating a PIK accrual or a warrant conversion can lead to significant financial disputes.

System Capabilities: The Hybrid Model leverages professional loan servicing systems that are specifically designed to handle these complex structures. They can automate the calculation of PIK interest, track multiple tranches of debt within a single facility, and manage complex waterfall distributions.

Covenant Monitoring: The system can also track financial covenants (e.g., Debt Service Coverage Ratio, Loan-to-Value) and alert the lender to potential breaches. This proactive monitoring is essential for preventing defaults and managing portfolio health.14

Chapter 6: The Technology Backbone – Portals, Data, and Integration

6.1 The Borrower Portal as a Competitive Advantage

In the digital age, borrowers expect a seamless online experience. They want to be able to log in to a portal to check their loan balance, download a statement, or request a draw—just as they would with a major bank.

Brand Extension: The Bedrock Core™ offering includes a branded Lender Portal.22 This is a critical feature. It allows the lender to offer a sophisticated digital interface without having to build it from scratch. To the borrower, the portal looks and feels like the lender's own proprietary technology, reinforcing the brand and projecting an image of scale and professionalism.

Self-Service: Portals enable self-service for routine tasks (e.g., retrieving a 1098 form or checking a due date). This reduces the administrative burden on the lender's staff, freeing them up for high-value interactions.22

6.2 Data Integration and Reporting

Data is the lifeblood of the modern lender. However, data is often trapped in silos—loan data in one system, accounting data in another, and CRM data in a third.

API Connectivity: Modern servicing platforms utilize APIs (Application Programming Interfaces) to connect with other systems. This allows for the seamless flow of data between the servicing platform and the lender's other tools (e.g., Salesforce, QuickBooks, or a data warehouse).38

Customizable Reporting: The Hybrid Model moves beyond static PDF reports. It offers "dashboards, loan-level views... and exception/work visibility".22 This allows the lender to slice and dice the portfolio data to answer specific questions: Which loans are maturing in the next 90 days? What is the concentration of exposure in a specific geography? Which borrowers have missed a payment?

6.3 Security and Data Privacy

As lenders handle sensitive borrower information (PII), data privacy and security are paramount.

Compliance: The partner assumes responsibility for maintaining the security of the platform, ensuring compliance with regulations such as GDPR or CCPA where applicable. This includes managing user access controls, encryption, and secure data storage.22

Chapter 7: Implementation – The Path to Partnership

7.1 The Onboarding Roadmap

Transitioning to a hybrid model is a significant strategic move. It is not a simple "plug and play" software installation; it requires a structured onboarding and migration process. The proposal 22 outlines a clear path to ensuring a successful transition.

Phase 1: Discovery and Data Mapping The most critical step is "loan onboarding and boarding support".22 This involves:

Data Validation: Reviewing the existing loan data (often from spreadsheets or legacy systems) to ensure accuracy. This "data cleansing" is vital to prevent historical errors from being migrated into the new system.

Mapping: Mapping the lender's specific data fields and loan products to the partner's system. This ensures that unique loan features are captured correctly.

Phase 2: Workflow Definition (SOPs)

The lender and partner must define the "Rules of Engagement." This involves documenting the Standard Operating Procedures (SOPs) for every interaction:

Who authorizes a draw request?

What is the escalation path for a delinquent borrower?

Who approves the monthly servicing report?

How are exceptions handled? This clarity is essential to ensure that the "Front Office" and "Back Office" operate in sync.22

Phase 3: Cutover and Go-Live

The definitive moment where the "system of record" shifts from the spreadsheet to the platform. This typically involves a "blackout period" where data is frozen, migrated, and then reconciled to the penny before the new system goes live.

7.2 The Ongoing Partnership Agreement

The relationship is governed by a Master Servicing and Services Agreement (MSSA).22 This document is as much of a legal contract as it is a dynamic operational framework.

Service Level Agreements (SLAs): The MSSA defines the performance expectations, including "System availability," "Incident management," and "Reporting cadence".22 These SLAs hold the partner accountable for delivery.

Scalability and Flexibility: The agreement is designed to evolve. As the lender enters new asset classes (e.g., moving from residential fix-and-flip to commercial bridge loans) or requires new capabilities, the platform can adapt. "Extraordinary servicing/workouts" or "bespoke integrations" can be handled via separate Statements of Work (SOWs), ensuring the core service remains efficient while allowing for customization.22

Conclusion: The Future of Private Lending is Hybrid

The landscape of private credit has evolved irrevocably. The era of the "Generalist" private lender—who sources, underwrites, services, and accounts for loans using a small team and a spreadsheet—is drawing to a close. The market has become too large, too complex, and too scrutinized for such operational fragility.

Conversely, the era of the "Black Box" outsourcer is also fading. Modern lenders refuse to cede control of their most valuable asset: the borrower relationship. They understand that in a commoditized capital market, the borrower experience is the product.

The Hybrid Technology-Enabled Servicing Model represents the synthesis of these two worlds. It offers a "best of both worlds" solution:

Control: The lender retains the brand, the borrower relationship, and strategic decision-making authority.

Ease: The partner handles the heavy lifting of loan accounting, data integrity, and operational workflow.

Advisory Support: The partner acts not just as a vendor, but as a strategic ally—a team of "former commercial banking operations professionals" 22 who guide the lender toward institutional best practices and operational excellence.

For the private lender looking to scale from $50 million to $500 million and beyond, this model is not merely an operational choice; it is a strategic imperative. It provides the Bedrock upon which a scalable, durable, and profitable lending franchise can be built—one that is capable of navigating the complexities of the modern financial landscape with confidence and precision.

%201-p-500.png)

.avif)